ETHDenver Games! SEC's Securities, Discord’s Stages, & Starbucks' Stamps

ETHDenver Games! SEC's Securities, Discord’s Stages, & Starbucks' Stamps

Bits of Signum | 2.21.23

Please let us know if you will be at ETHDenver March 1st-5th as Signum Growth will be hosting a few exciting gaming activities such as an investor + game developer brainstorm on Web3 + AI Driving to the Next Cycle Beyond F2P (Free To Play games). First, we cover some highlights of the SEC hammer that came down over the last week, and then one notable item in gaming (Discord’s important Stage product is a glimpse into the future) and one in digital assets (Starbucks’ NFTs sold for dollars, not crypto, fly off the coffee bar.)

SEC’s First Strike Against Crypto - Staking as a Service

Several weeks after Gemini and Genesis Global Capital were charged with the sale of unregistered securities (a yield product) through Gemini Earn, the SEC has declared Kraken’s staking-as-a-service program as an unregistered securities offering and has shut it down. Kraken’s staking service was terminated, and all 22 tokens’ balances have been redeposited into customers’ wallets (aside from Ethereum, which will be unlocked after the Shanghai upgrade.) Additionally, Kraken will pay a $30 million fine, and has been summoned by the IRS to bring forth customer documents spanning 2016 to 2020. We believe that all of these actions reflect the SEC’s mantra to exchanges - “Come in and register (as US exchanges).” Side note: Joshua Ashley Klayman and I were on the Space Monkeys podcast out yesterday explaining our views here.

Context: Polkadot, Ethereum, Tezos and others are “Proof of Stake” networks. Using Polkadot as an example, participants who are staking have locked up their tokens for 28 days to provide the function of securing the network. In other words, the community and its locked tokens provide the security that is core to what Polkadot offers developers. In exchange, participants receive new tokens to make sure that they are whole at the end of the lock up period (i.e. so that they do not experience dilution.) Platforms like Kraken have emerged that offer staking-as-a-service by pooling tokens from many people together and providing this function as a service.

While Gemini Earn and Kraken’s staking services differ in title and methodology, Gensler said “It's not about the labels, it's about the underlying economics.” The concern is what could be happening that is not disclosed - could Kraken be trading the tokens or depositing them in high-risk DeFi apps instead of staking them? As a rule of thumb, in our opinion, it's important to look at the activity that is happening, the function of such activity, and the fund flows around it. If activities look to the average person like investment contracts, they probably are. If the activity looks like it serves a function for the underlying network, as long as it is correctly and accurately presented, it should be in a different category. Finally, the SEC is calling out pooling of customer assets and liquidity mismatches. If Polkadot’s unbonding (lock) period is 28 days, and yet customers can have full liquidity on Kraken, what is the risk in this liquidity mismatch (i.e., “a run on the bank”) and where is that explained?

We mentioned in January that we felt Coinbase was lucky to get the SEC guidance via a Wells notice before they launched the Coinbase Earn product, skipping the fine and all of the trouble that Gemini had to go through with the SEC. Similarly, with staking-as-a-service, Coinbase is able to learn from the fine that Kraken has paid. However, instead of falling in line on this guidance, it appears that Coinbase has put a stake in the ground (no pun intended) as the entity who might lead in the crypto industry’s efforts to change the existing laws. Chief Legal Officer Paul Grewal tweeted “these products are basically yield products. True on-chain staking services like ours are fundamentally different…our customers’ rewards are tethered to realities. They depend on the rewards paid by the protocol and commissions that we disclose.”

Side note: It is worth noting that the work that we did as advisors to the Web3 Foundation on the launch of Polkadot, by following the guidance on morphing, was just one way, not the only way, to find a regulatory compliant path. Another way is to change the US federal securities laws. Back in 2019, we were simply looking for the lowest friction way, when the primary goal was to deliver the Polkadot network. We concluded that working within the existing laws would be easier than trying to change the laws by going to Congress, which could take years. As a reminder, the job of the SEC is enforcement, or to enforce existing laws, not to change the laws.

The SEC’s Second Strike Against Crypto - Stablecoins (Terraform Labs & Paxos)

Above are the top 10 “stablecoins” by “market cap”. While stablecoins aim to bring a fiat-pegged currency to the blockchain, their issuers provide varying levels of collateral and transparency. Post Terra & FTX, the SEC seems determined to filter out the instability in stablecoins and to punish those who have not provided clear communications and disclosures around what exactly people are buying. The risk in not doing so can result in clear harm to retail investors, as the SEC argues was the case in Terraform Labs.

On Thursday, the SEC officially charged Terraform Labs and Do Kwon with multi-billion dollar crypto asset securities fraud. The allegations center around a suite of cryptocurrencies, including LUNA, algorithmic-stablecoin UST, and various “mAssets,” which are cryptocurrencies that mirrored US Stocks in an attempt to simulate equity trading on-chain. According to the SEC, Terraform Labs and Do Kwon repeatedly misled investors about UST’s stability and marketed it as a “yield-bearing” stablecoin. Also, the issuer told investors that LUNA would directly accrue value from a Korean mobile app using the Terra blockchain. The most concerning allegation is that “Terraform and Kwon also allegedly misled investors about the stability of UST. In May 2022, UST depegged from the U.S. dollar, and the price of it and its sister tokens plummeted to close to zero.” The case states that TerraUSD’s stability was consciously fabricated, putting the severity of the allegations in line with the FTX case in our view. Do Kwon and Terraform labs allegedly “secretly discussed with a third party that the third party would purchase massive amounts of UST to restore the $1.00 peg.” The “restoration” worked and then they dishonestly thanked the “algorithm” as if it somehow the technology was built as originally intended. All that comes to mind is mind blown.

There is a very articulate thread on Twitter asking if the SEC is saying that UST is a security because it can be exchanged for a yield bearing instrument, and by extension, wouldn’t this make fiat a security? Our initial response - nah, it is probably the promised yield on UST by Terraform Labs that makes it a security, not that it can be exchanged for a security.

Finally, Paxos was ordered by the The New York Department of Financial Services (NYDFS) to stop issuing the stablecoin Binance USD (BUSD). According to the Wall Street Journal, the company may also be sued by the SEC over allegedly violating investor protection laws by issuing BUSD as an unregistered security. While the issuance of new BUSD will cease today, February 21, the company will continue to service the product and manage redemptions in USD and USDP (US dollar-backed stablecoin Pax Dollar) until at least February 2024. Paxos stated that USDP and Pax Gold (PAXG) remain unaffected by the NYDFS order. USDP is currently the 6th largest stable by market cap, albeit Tether being 80x its size.

Now let’s return to the (much more fun) world of digital assets!

Discord Stage Channels Taking Center Stage

Discord’s Stage channels, which are used to run community events, can now support video, screen sharing, and text chat. Any Discord server with the "community" feature set to enabled has the ability to use video or screen share in Stage channels with up to 50 audience members. Servers with Tier 2 or Tier 3 Server Boosting can expand their capacity for using video in Stage channels for up to 150 or 300 viewers respectively. Up to five members may use video on Stage, and one screen share is supported on a Stage channel at a time. The presenter sharing their screen can be different from the five others using video, and audience members won't have their own audio or video feeds broadcast to the community without permission. Text chat in Stage channels will work just like it does in Voice channels.

We’ve always believed that Zoom is an early iteration of the metaverse, but unlike Discord, it lacks the behavioral foundation of building and sustaining communities. With this video upgrade to Stages, Discord has just transformed into a fully-fledged digital communications platform across text, channels, screen-sharing, and video. While not as many people can participate in video as Zoom (yet), it's a significant shift in the platform's offering and a positive glimpse into its future offering.

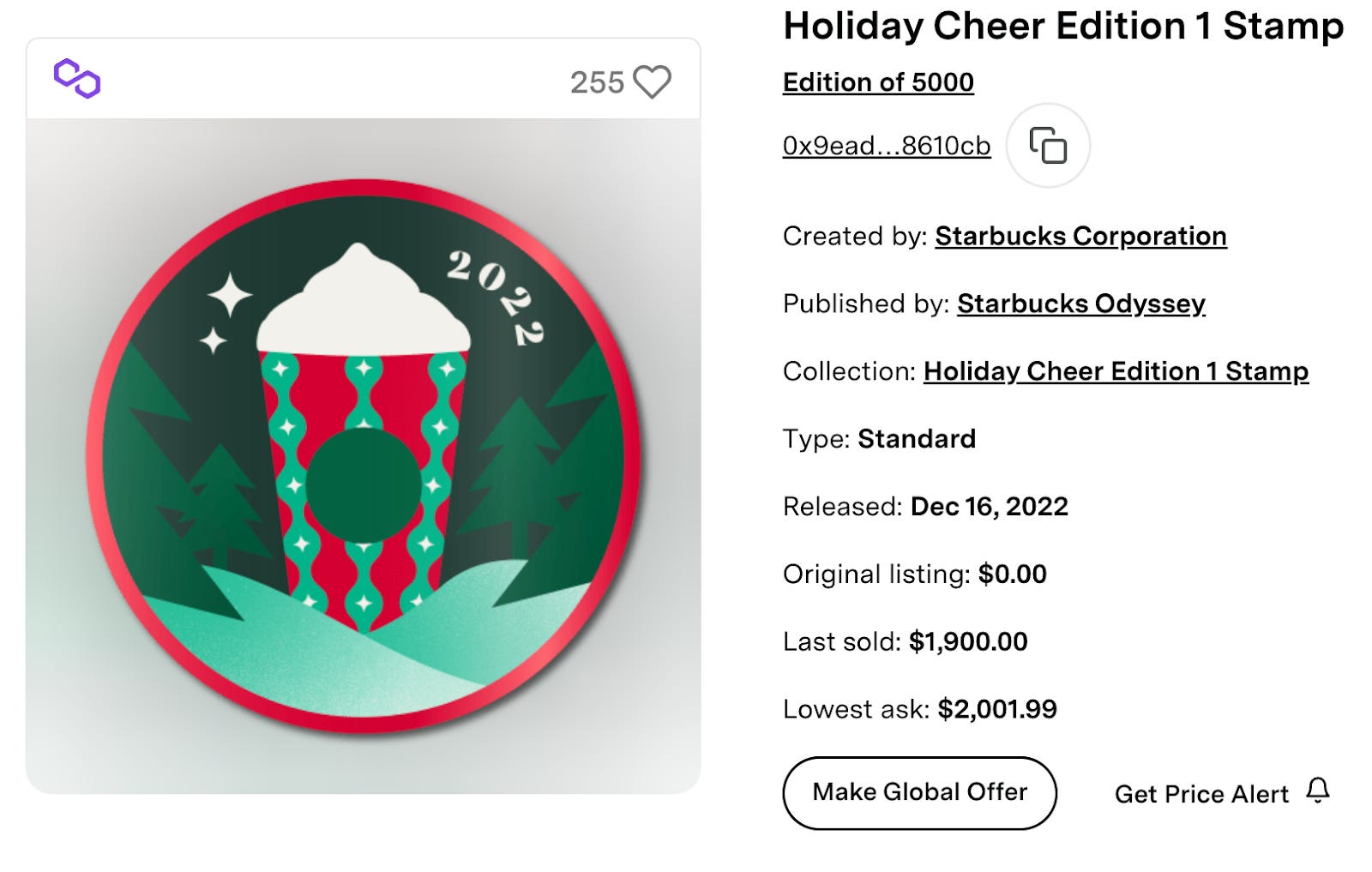

Starbucks Odyssey’s digital asset caught our attention because it was denominated in fiat, payable by credit card, not crypto, and the interest and behavior was still there! Since the Beta launch of Starbucks Odyssey in December, the NFT-backed loyalty program has released 45,000 NFTs called Stamps, which were awarded to members for buying certain drinks, items, and completing minigames. In total, the secondary market volume for these Stamps has hit $143,000. The first of the four NFTs released, "Holiday Cheer Edition 1 Stamp," has accounted for 80% of the total USD volume and ~40% of total trades completed. Also, 151 of these Cheer Edition 1’s have traded hands at an average price of ~$880. It will be notable to watch this budding collector community within the Starbucks membership program, as no in-app rewards were tradable prior to this.

Thanks for reading if you are still with us, and see you at ETHDenver!